Shot:

Chaser:

Chaser:

Single-Payer Healthcare System Projected to Send Colorado Off a Financial Cliff

[Hat Tip: FoIB Holly R]

Single-Payer Healthcare System Projected to Send Colorado Off a Financial Cliff

[Hat Tip: FoIB Holly R]

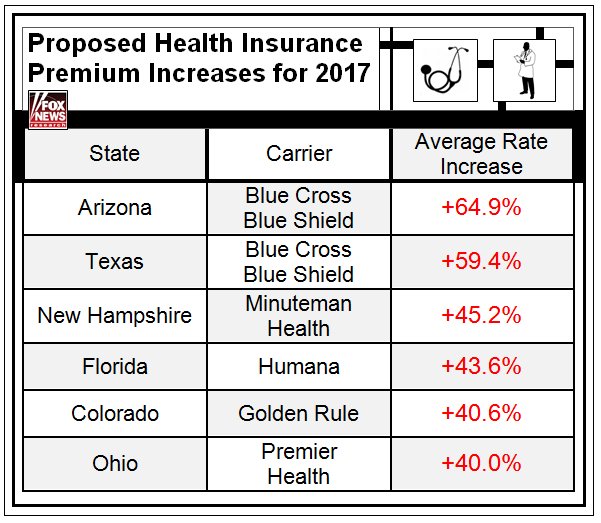

Five insurance companies that had offered coverage in the Affordable Care Act marketplace have told state regulators that they will opt out or scale back coverage when the next open season for Affordable Care Act coverage begins Nov. 1.

There will still be coverage, but with fewer providers, experts say costs will likely go up “much higher in 2017 than they had in the past couple of years.”- AZ CentralCosts will likely go up.

A national estimate by the Kaiser Family Foundation predicts that premiums for one of the lower-costs plans could rise as much as 9 percent next year, compared to 2 percent this year. In Arizona, those higher premiums could hit more than 100,000 people.

Jennings is one of more than 250 brokers certified to help customers navigate the state exchange, Access Health CT, and find the plan that best fits their needs. But next year, she said, she won’t be helping customers anymore if the health insurers on the exchange decide to eliminate the already-low commissions they pay to brokers like her.

As state regulators consider rate proposals for next year, both of the carriers set to remain on Connecticut's exchange – Anthem and ConnectiCare – could eliminate their commissions for brokers in 2017, creating uncertainty as brokers and customers plan for the coming year. Anthem said earlier this year it would eliminate broker commissions while ConnectiCare has yet to decide. - CT MirrorConnecticut is not the only state where agent commissions have been cut to zero. Carriers have been decreasing commissions for the last 3 years with major cuts in the last 18 months.

Written in Obamacare, transitional reinsurance is a fee disguised as a levy on insurance companies that is passed through to all consumers. It is a temporary program that cost each covered person a set annual dollar amount. In 2014 every insured person was charged $63. This reduced to $44 in 2015 and is set for $27 in 2016.

Written in Obamacare, transitional reinsurance is a fee disguised as a levy on insurance companies that is passed through to all consumers. It is a temporary program that cost each covered person a set annual dollar amount. In 2014 every insured person was charged $63. This reduced to $44 in 2015 and is set for $27 in 2016.

The Department of Health and Human Services just "found that the ACA's Medicaid expansion enrollees cost an average of $6,366 in (fiscal) 2015--49 percent higher than the $4,281 amount that the agency projected in last year's report." - Maciver InstituteHow can they miss by that much?